Skip to content

Skip to content

VA loan calculator: Your key to understanding VA loans! Dive into benefits like no PMI and how to make smart choices in your home-buying journey.

VA Loan Calculator

Home Value

–

Down Payment

–

Interest Rate

–

Loan Term

–

VA Specifics

–

Monthly Payment

–

| Parameter | Value |

|---|---|

| Home Value | – |

| Down Payment | – |

| Interest Rate | – |

| Loan Term | – |

| VA Specifics | – |

| Loan Amount | – |

| Monthly Payment | – |

| Total Payment | – |

| Total Interest Paid | – |

Table of Contents

VA loans are a financial solution specifically designed for veterans and active-duty service members offering benefits like no down payment lower interest rates, and no PMI requirements.

This comprehensive guide explores the features of VA loans how to use a VA loan calculator, and the key factors influencing loan amounts and payments.

Learn how understanding home value down payment options, and interest rates can help you make informed decisions in your home buying journey.

Discover the advantages of VA loans and how they make homeownership accessible and affordable for those who have served in the military.

Introduction to VA Loans

VA loans are a specialized financial product designed to assist eligible veterans active-duty service members, and certain members of the National Guard and Reserves in purchasing homes.

These loans are backed by the U.S. Department of Veterans Affairs (VA), which allows lenders to offer favorable conditions that are not typically available through conventional mortgage options.

As a result, VA loans have become an increasingly popular choice among those who have served in the military offering unique benefits that cater to their needs.

One of the most notable features of VA loans is the absence of a down payment requirement.

Unlike conventional loans that often require a substantial initial investment, eligible borrowers can finance 100% of the home’s purchase price.

This significant advantage makes homeownership more accessible for service members and veterans, easing the financial burden associated with buying a home.

Moreover, VA loans typically offer lower interest rates compared to conventional loans as they are insured by the VA This leads to lower monthly payments and long-term savings for borrowers.

Additionally, there are no private mortgage insurance (PMI) requirements with VA loans, further reducing the overall cost of the loan.

These financial benefits are critical, considering that many veterans may transition to civilian life with varying degrees of financial readiness.

The VA loan program also provides flexibility in terms of credit requirements, which can be beneficial for those who may have experienced financial challenges.

While lenders will still assess a borrower’s creditworthiness, the guidelines for VA loans are generally more lenient than those for conventional mortgages.

In essence, VA loans are designed to honor the sacrifices of veterans and service members by making homeownership feasible and affordable.

Their unique features, such as no down payment, favorable interest rates, and flexible credit requirements, constitute a valuable resource for those who have served in the armed forces.

What is a VA Loan Calculator?

A VA loan calculator is a specialized financial tool designed to assist eligible veterans and service members in estimating the costs associated with obtaining a VA loan.

This calculator simplifies the often complex mortgage process by providing potential borrowers with insights into their financing options, enabling them to make informed decisions regarding their home purchases.

The core function of a VA loan calculator is to project monthly mortgage payments based on several factors including the loan amount, interest rate loan term, and the applicant’s down payment.

Additionally, it considers the unique benefits associated with VA loans, such as the absence of private mortgage insurance (PMI) and favorable interest rates.

These features make the calculator an invaluable resource for veterans looking to understand their financial commitments.

Beyond estimating monthly payments, a VA loan calculator also offers projections of the total costs involved over the life of the loan.

This encompasses not only principal and interest but also property taxes, homeowners insurance, and any applicable funding fees specific to VA loans.

By inputting various scenarios such as different home prices or down payment amounts borrowers can visualize how changing their financial parameters impacts their overall expenditure.

In essence, the VA loan calculator serves as a practical guide, helping veterans and active-duty personnel navigate the financial landscape of home ownership.

Its user-friendly interface allows borrowers to quickly and efficiently assess their options, ensuring that they can evaluate their readiness to commit to a VA loan.

By utilizing such a tool, potential home buyers can gain clarity on what they can afford and identify the best financing strategies to meet their individual needs.

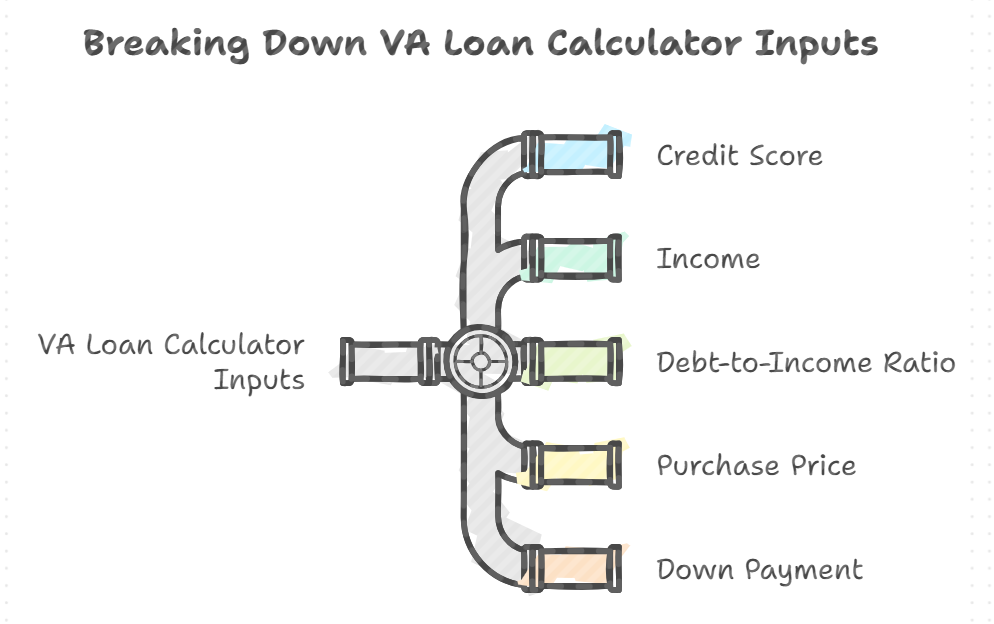

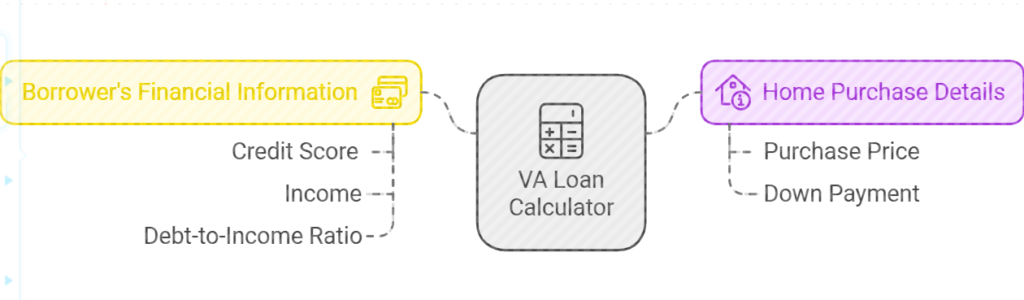

Key Inputs for the VA Loan Calculator

When utilizing a VA loan calculator, several crucial inputs are necessary to determine the most accurate representation of potential loan costs.

Understanding these inputs can greatly enhance the decision-making process for veterans and active service members seeking to secure a home loan.

The first essential input is the home value. This refers to the price of the property you wish to purchase. For example, if you are considering buying a home valued at $300,000, this figure will serve as the foundation for your calculations.

The total loan amount is generally equivalent to the home value unless you are planning to make a down payment.

Next, the down payment acts as another key input. Fortunately, VA loans typically do not require a down payment, but if you do choose to make one, it will directly reduce your loan amount.

For instance, a down payment of $15,000 on a $300,000 home leaves a loan balance of $285,000. This modification in principal can result in significant savings over the loan’s lifetime.

The interest rate is another critical factor in the calculation. This rate can vary based on market conditions and your creditworthiness.

For example, a 3.5% interest rate compared to a 4.5% interest rate will affect your monthly payments and the overall cost of the loan.

The duration of the mortgage, referred to as the loan term, is another vital input. VA loans often have terms of 15, 20, or 30 years, with longer terms generally resulting in lower monthly payments but potentially higher overall interest costs.

Finally, specific VA loan requirements, such as funding fees or circumstances that necessitate consideration of residual income, are integral as well.

These elements are critical in finalizing the calculations, ensuring borrowers are well-informed of their options and obligations.

Understanding Home Value and Its Impact

The value of a home plays a crucial role in determining the loan amount and monthly payments for a VA loan. When applying for a VA loan, it is essential to understand how home valuation affects the borrowing process.

The key aspects involved in understanding home value include the concepts of appraisals and market value, both of which are vital to ensure a smooth loan application experience.

Appraisals are conducted by licensed professionals who assess the property’s value based on various factors such as location, size, condition, and comparable sales in the neighborhood.

For VA loans, an appraisal is required to guarantee that the home meets minimum property requirements established by the Department of Veterans Affairs.

This appraisal helps ensure the veteran is not overpaying for the home and helps lenders mitigate risks associated with the loan.

Market value reflects the current price at which the property is likely to sell, based on the local real estate market conditions. It is influenced by supply and demand, interest rates, and economic factors.

The relationship between the market value and the loan amount is particularly significant, as lenders typically limit financing to a percentage of the appraised value or the purchase price, whichever is lower.

For instance, if a home is appraised at $300,000 and the purchase price is $320,000, the lender will likely base the VA loan amount on the lower appraised value of $300,000.

Consequently, this affects the monthly payments, making it essential for borrowers to understand how these values interplay when planning their home purchase.

Accurately assessing a home’s value can ultimately lead to more informed financial decisions throughout the VA loan process.

Evaluating Down Payment Options

When considering a VA loan, one of the critical factors to assess is the down payment option.

While VA loans are well-known for their unique feature of allowing qualified veterans and service members to purchase homes without a down payment, there are several implications associated with both no down payment and partial down payment scenarios that homebuyers should evaluate thoroughly.

Choosing to forgo a down payment can provide immediate financial relief. It allows borrowers to retain their savings for other essential expenses, such as moving fees, home repairs, or emergency funds.

Moreover, without a down payment, first-time homebuyers can enter the housing market much faster. However, this option may lead to higher monthly payments as the loan amount will be significantly higher compared to a scenario where a down payment is made.

On the other hand, contributing a down payment can have considerable long-term advantages.

Making a partial down payment can reduce the total loan amount, resulting in lower monthly payments and potentially decreasing the amount of interest paid over the loan term.

Additionally, a larger down payment may enhance the borrower’s creditworthiness in the eyes of lenders, opening up opportunities for better interest rates.

Furthermore, in some cases, putting money down can mitigate the need for private mortgage insurance (PMI), bringing additional savings to homeowners.

It’s important to explore various down payment strategies in line with individual financial circumstances and goals. One approach is to consider a down payment that is sizeable enough to balance the benefit of lower monthly payments against the need for accessible cash reserves.

Each choice carries its own benefits and costs, making it imperative for potential borrowers to evaluate what best aligns with their financial strategy and overall homeownership plans.

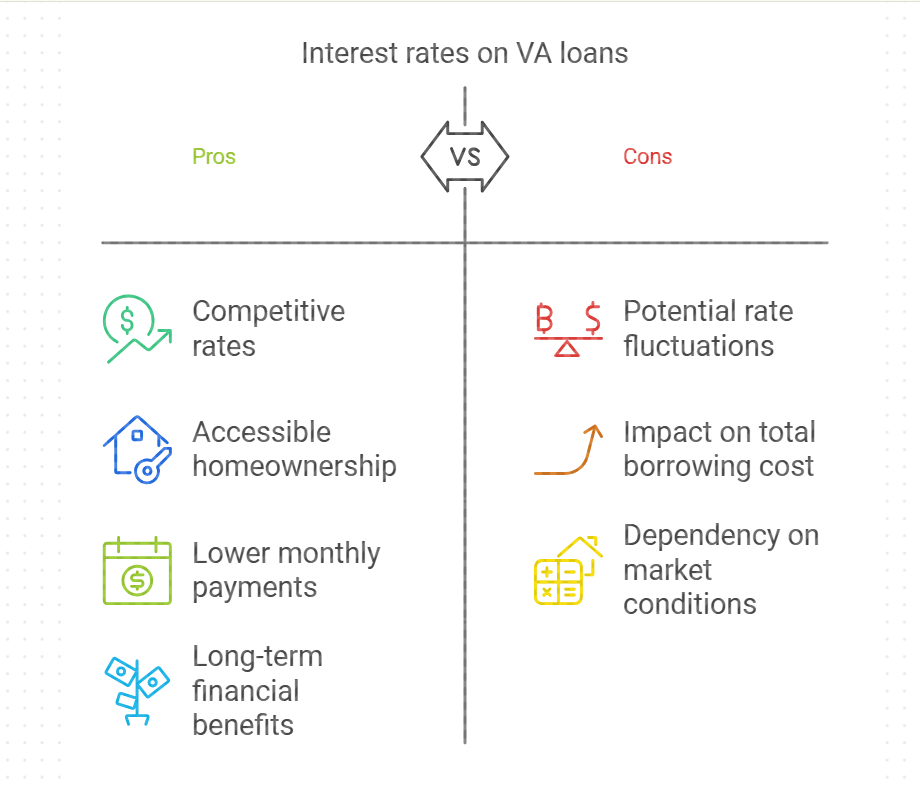

Interest Rates and Their Role in VA Loans

Interest rates are a critical component of any loan, including VA loans, which are designed to assist veterans and active-duty service members in obtaining home financing with favorable terms.

The interest rate applied to a VA loan can significantly influence the overall cost of borrowing and ultimately affect a borrower’s financial situation.

Generally, VA loan interest rates are competitive and often lower than those of conventional loans, making them an appealing option for eligible borrowers.

The determination of interest rates for VA loans hinges on various factors, including market conditions, lender policies, and individual borrower profiles.

Lenders assess current economic indicators and adjust their rates accordingly, while also taking into account the specific attributes of the borrower, such as credit score and overall loan amount.

A higher credit score typically corresponds with lower interest rates, as it indicates a stronger likelihood of timely payment.

Maintaining a good credit score is therefore essential for borrowers looking to secure the best possible terms on their VA loans.

Furthermore, interest rates can affect the total payments made over the life of the loan. A small difference in the interest rate can result in significant savings or expenses when projected over several years.

For instance, a borrower with a lower rate may see a noticeable reduction in their monthly payments, making it easier to manage their budget. Conversely, a borrower facing higher rates could encounter additional financial strain.

Thus, understanding how these rates are determined and the importance of credit scores can empower prospective VA loan recipients to make informed financial decisions.

By navigating these factors effectively, borrowers can maximize the benefits of their VA loans and secure a favorable financial outcome.

Loan Terms: What You Need to Know

When considering a VA loan, understanding loan terms is crucial, as they play a significant role in determining payment schedules and the accumulation of interest.

Loan terms typically refer to the duration over which the borrowed amount must be repaid.

VA loans commonly offer two primary term lengths: 15 years and 30 years. Each option presents distinct advantages and disadvantages, influencing your overall financial landscape.

A 15-year VA loan allows borrowers to pay off their mortgage in half the time compared to a 30-year loan.

This shorter loan term often comes with lower interest rates, resulting in reduced total interest paid over the life of the loan. Additionally, homeowners can build equity more rapidly, offering them a greater ownership stake in their property sooner.

However, the monthly payment amounts are generally higher due to the shorter repayment period, which may strain the monthly budget for some borrowers.

Conversely, a 30-year VA loan spreads the payments over a longer duration, creating lower monthly payments.

This extended repayment period can ease financial pressure for many borrowers, making homeownership more accessible.

However, while monthly payments may be lower, the total interest paid over the life of the loan accumulates significantly, making it a costlier option in the long run.

Moreover, it may take longer to build equity in the home, potentially affecting an owner’s flexibility regarding refinancing or selling the property.

Ultimately, selecting the right loan term depends on individual financial situations, goals, and tolerance for risk.

By weighing the pros and cons of each option, borrowers can make more informed decisions that align with their unique circumstances and long-term financial wellness.

Calculating Loan Amounts and Payments

The VA loan calculator serves as an indispensable tool for veterans seeking to determine their potential mortgage obligations.

To utilize this calculator effectively, one must begin by entering the desired home price, which serves as a baseline for the calculations. For example, if the home value is set at $300,000, the calculator will use this figure as the primary input.

Next, consider the down payment, a crucial component of any loan calculation. VA loans typically do not require a down payment, but for scenarios where a down payment is applicable, users can input varying amounts.

Supposing a down payment of $20,000 is made on the previously mentioned $300,000 home price, the adjusted loan amount would be $280,000, which the calculator will utilize for further computations.

Interest rates play a pivotal role in determining monthly payments. The calculator allows users to input different interest rates to assess their impact on overall payments.

For instance, if the interest rate is at 3%, the monthly payment for a $280,000 loan term of 30 years would approximately equate to $1,178.

By contrast, tweaking the interest rate to 4% would increase the monthly payment to roughly $1,333, illustrating how sensitive loan payments can be to interest variations.

Lastly, the terminal input is the loan term commonly set at 15 or 30 years. The length of the loan will significantly affect the monthly payment and total interest paid over the life of the loan.

For the previously explored example, choosing a 15-year term instead of 30 years will yield a higher monthly payment, albeit significantly reducing the total interest paid.

Utilizing the VA loan calculator effectively enables veterans to gain a clear understanding of their loan amounts and monthly obligations, allowing for informed financial decisions in their home-buying journey.

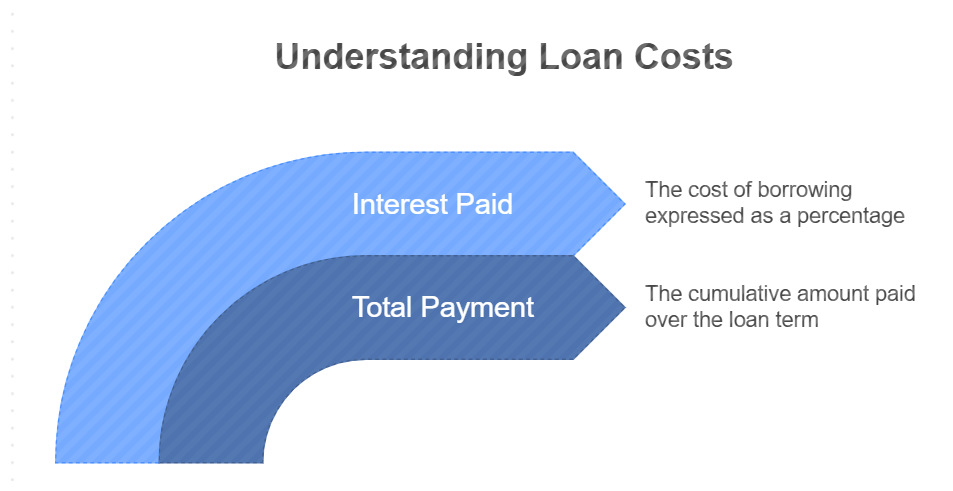

Total Payment and Interest Paid Over the Life of the Loan

Understanding the total payment and total interest paid over the life of a VA loan is crucial for potential borrowers. This knowledge allows individuals to make informed financial decisions and plan accordingly for the future.

The VA loan calculator serves as a valuable tool in this regard, offering a clear breakdown of these essential components.

To calculate the total payment over the life of the loan, one must consider the loan amount, interest rate, and the loan term.

Typically, VA loans come with favorable terms, including no down payment and competitive interest rates. However, it is essential to input precise values into the VA loan calculator to obtain accurate figures.

The calculator provides an estimate of the monthly payment, which can then be multiplied by the total number of payments (months) to yield the total payment.

For example, if a borrower takes out a VA loan for $300,000 at a 3% interest rate for 30 years, understanding the computed monthly payment is the first step to gauging the overall financial commitment.

In addition to total payments, assessing the total interest paid over the life of the loan is critical. This figure can significantly impact long-term financial health.

The VA loan calculator facilitates this assessment by breaking down interest alongside the principal amount. As an example if the total interest for the $300,000 loan over 30 years amounts to $155,000, borrowers can evaluate whether they are comfortable with this long-term expense.

By recognizing both total payments and interest, borrowers can devise strategies to minimize costs, such as making extra payments or refinancing if interest rates drop.

A comprehensive understanding of total payment and interest paid enables borrowers to navigate their VA loan more effectively, ultimately leading to better financial planning and decision-making.

Look at this calculator for more details

VA Loan Calculator

| Parameter | Value |

|---|---|

| Loan Amount | — |

| Total Mortgage Payments | — |

| Total Interest | — |

| Mortgage Payoff Date | — |

| Monthly Principal and Interest | — |

Conclusion

The VA Loan Calculator is an essential tool for anyone considering a VA loan. With its user-friendly interface, accurate calculations, and detailed breakdown it provides valuable insights into the financial implications of your loan.

Whether you’re a first-time homebuyer or a seasoned investor, the VA Loan Calculator can help you make informed decisions and plan your budget effectively.

Use the calculator today to take the first step toward owning your dream home!

Here are other calculators maybe you need in your life

Caloric Intake Calculator for Weight Loss: Discover how many calories you need daily to shed pounds effectively. Personalize your plan now!

Age Calculator By Minutes: Find your age in years, months, days, hours, and minutes. Easy-to-use tool for precise time tracking.

VA Mortgage Calculator: Easily estimate your monthly payments with our tool, perfect for veterans exploring VA loans. Enjoy no PMI and low interest rates!

RRSP Future Value Calculator: The RRSP Future Value Calculator serves as a valuable resource for individuals aiming to enhance their retirement savings strategies

Body Fat Calculator + Ovulation Percentage Calculator: this is for women

VA Loan Calculator: Whether you’re a first-time homebuyer or a seasoned investor, the VA Loan Calculator can help you make informed decisions and plan your budget effectively

VA Loan Calculator: Understanding Key Features and Benefits